Many business owners struggling with Merchant Cash Advance (MCA) debt ask whether they can legally stop MCA payments. When daily or weekly withdrawals begin disrupting cash flow, it can become difficult to cover payroll, vendors, and other operating expenses. While businesses may have options depending on their situation and contract terms, stopping payments without a clear strategy can trigger defaults, collection activity, additional fees, or legal disputes. Understanding your MCA agreement and exploring available relief options can help you make informed decisions before the situation becomes more difficult to manage.

Get an Instant Payment Reduction Quote

Why Businesses Consider Stopping MCA Payments

Most business owners do not set out to stop their MCA payments. In many cases, they reach that point after months of struggling to keep up with daily or weekly withdrawals. What once seemed like manageable payments can become overwhelming when revenue declines, expenses increase, or multiple funding obligations begin competing for the same cash flow.

As financial pressure grows, business owners often look for ways to create immediate breathing room. Stopping MCA payments may appear to be the fastest solution, especially when basic operating expenses take priority. Common reasons businesses consider stopping payments include:

- Difficulty covering payroll

- Falling behind on vendor payments

- Frequent overdrafts and bank account shortages

- Seasonal declines in revenue

- Multiple stacked MCA obligations

- Insufficient working capital for daily operations

For many businesses, the real issue is not a single payment. The problem is a broader cash flow imbalance that continues to worsen over time. Understanding why payment struggles occur is the first step toward finding a solution that addresses the underlying problem rather than simply delaying it.

What Happens If You Stop Making MCA Payments?

Stopping MCA payments can trigger a series of consequences that often extend beyond the missed payments themselves. Most MCA agreements contain default provisions that give the funding company additional rights when a business fails to meet its obligations. While the exact outcome depends on the contract and circumstances, ignoring payments rarely makes the underlying debt disappear.

After a default, businesses may face collection efforts, increased communication from the funder, additional fees, or legal action. Cash flow problems can also worsen if the situation remains unresolved. The earlier a business addresses payment challenges, the more options it typically has available. Rather than waiting for the problem to escalate, many owners benefit from reviewing their agreements and exploring potential MCA relief solutions before defaults create additional financial pressure.

Legal Risks of Stopping MCA Payments

Before stopping MCA payments, business owners should understand the potential legal risks involved. Most Merchant Cash Advance agreements contain specific provisions that outline what happens when payments stop or an account falls into default. While every contract differs, funders often have legal remedies available when a business fails to meet its obligations. Taking action without fully understanding the agreement can create additional financial and legal pressure.

Depending on the terms of the MCA contract, businesses may face collection efforts, breach of contract claims, court proceedings, or other legal actions. Some agreements also include provisions that can accelerate repayment obligations after a default. The legal risks often increase when businesses stop payments without a clear strategy or professional guidance. Reviewing the agreement carefully and exploring available relief options can help business owners make informed decisions before a difficult situation becomes even more complicated.

How ACH Authorizations Affect MCA Payment Collection

Most MCA companies rely on ACH authorizations to collect payments directly from a business bank account. When a business signs an MCA agreement, it typically grants the funder permission to initiate automatic withdrawals according to the repayment terms. This process allows payments to occur without manual action from the business owner, which makes collection faster and more consistent for the funding company.

Because ACH withdrawals happen automatically, they can have a significant impact on day-to-day cash flow. Business owners may not feel the pressure immediately, but recurring withdrawals can become difficult to manage when revenue slows or expenses increase. A payment schedule that works during strong sales periods may become a challenge during slower months.

ACH authorizations generally allow MCA companies to:

- Collect payments automatically

- Reduce missed payment risk

- Withdraw funds on a daily or weekly schedule

- Monitor repayment activity more efficiently

- Maintain consistent payment collection

Understanding how ACH authorizations affect MCA payment collection can help business owners better evaluate the risks and responsibilities that come with MCA financing. The more you understand the repayment process, the better prepared you will be to manage cash flow and avoid financial surprises.

Can You Revoke an MCA ACH Authorization?

Many business owners facing cash flow challenges wonder whether they can revoke an MCA ACH authorization and stop automatic withdrawals from their bank account. While ACH authorizations may be revoked under certain circumstances, doing so does not automatically eliminate the obligations contained in the MCA agreement. The authorization governs how payments are collected, but the underlying repayment responsibility typically remains in place.

Before taking action, it is important to understand the potential consequences. Revoking an ACH authorization without a clear plan can trigger defaults, collection efforts, additional fees, or legal disputes. Every MCA agreement contains unique terms, and the impact of revoking an authorization can vary from one situation to another. Business owners should carefully review their contracts and explore available relief options before making changes that could create additional financial or legal challenges.

Alternatives to Stopping MCA Payments

If MCA payments are creating financial strain, stopping payments is not the only option. Many businesses have alternatives that may help relieve pressure while reducing the risk of defaults, collections, or legal disputes. The goal should be to address the underlying cash flow problem, not simply delay it. Taking action early often provides more flexibility and a wider range of potential solutions.

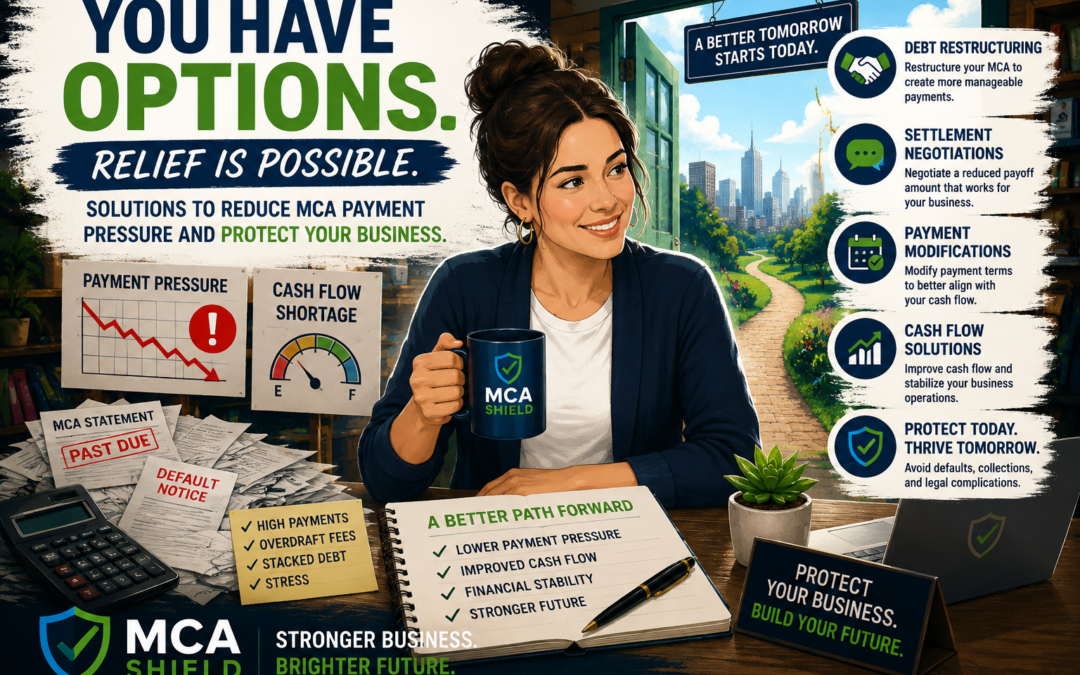

Depending on the situation, business owners may consider options such as MCA debt restructuring, settlement negotiations, payment modifications, or other relief strategies. These approaches can help create a more manageable repayment structure while allowing the business to continue operating. Exploring alternatives before a payment crisis develops often leads to better outcomes and more opportunities to regain financial stability.

How MCA Debt Restructuring May Reduce Payment Pressure

When MCA payments begin consuming too much of a company’s cash flow, MCA debt restructuring may provide a path toward greater financial stability. Rather than allowing payment pressure to continue building, restructuring focuses on creating a repayment arrangement that better aligns with the business’s current financial reality. For many owners, the goal is simple: create enough breathing room to keep the business operating while addressing existing obligations.

Every situation is different, but restructuring often aims to improve cash flow by reducing the immediate strain caused by aggressive repayment schedules. Lower payment pressure can make it easier to focus on running the business instead of constantly reacting to daily ach withdrawals and cash shortages.

Potential benefits of MCA debt restructuring may include:

- More manageable payment schedules

- Improved cash flow stability

- Reduced pressure on payroll and operating expenses

- Greater flexibility for vendor payments

- A clearer path toward long-term financial recovery

While restructuring is not a one-size-fits-all solution, it can provide meaningful relief for businesses struggling to keep up with MCA obligations. Taking action before cash flow problems become severe often creates more opportunities to stabilize the business and avoid deeper financial challenges.

Warning Signs It Is Time to Seek Professional Help

Many businesses try to manage MCA payment challenges on their own, but there comes a point when professional guidance may become necessary. The longer cash flow problems continue, the more difficult they often become to resolve. Recognizing the warning signs early can help business owners take action before defaults, collections, or additional funding create even greater financial pressure.

Common signs that it may be time to seek professional help include:

- Struggling to cover payroll or operating expenses

- Falling behind on vendor payments

- Taking new MCA funding to pay existing MCA obligations

- Facing collection calls or default notices

- Experiencing frequent overdrafts or cash shortages

- Managing multiple stacked MCA advances

If these issues sound familiar, it may be time to evaluate your options. Professional guidance can help identify potential solutions, reduce MCA payment pressure, and create a strategy for restoring financial stability before the situation becomes more difficult to manage.

Steps to Take Before MCA Payments Become Unmanageable

The first step is to gain a clear understanding of your financial situation. Review your MCA agreements, repayment schedules, and current cash flow. Look for patterns that may be contributing to the problem, such as declining revenue, rising expenses, or multiple funding obligations.

Consider taking the following steps:

- Review all current MCA obligations

- Analyze cash flow and operating expenses

- Identify areas where spending can be reduced

- Avoid taking additional MCA funding to cover existing debt

- Explore restructuring or relief options

- Seek professional guidance before defaults occur

The goal is not simply to survive the next payment withdrawal. The goal is to create a sustainable plan that allows your business to continue operating while addressing its existing obligations. Taking proactive steps today can help prevent much larger challenges tomorrow.

Success Stories from Our Clients

“Thanks to mcashield.com, we reduced our daily payments significantly and saved our business from financial distress.”

John D., Restaurant Owner

“The consolidation process was seamless, and now we can focus on growing our business instead of worrying about multiple payments.”

Emily R., Retail Store Manager

“I was skeptical at first, but mcashield.com delivered on their promise. Our cash flow has improved dramatically.”

Michael T., Small Business Owner