Choosing between a Merchant Cash Advance vs SBA Loan can have a major impact on your business’s cash flow and long-term financial health. While both options provide access to capital, they differ significantly in approval requirements, repayment terms, funding speed, and overall cost. Understanding these differences can help you determine which solution is the better fit for your business.

Get an Instant Payment Reduction Quote

Understanding Merchant Cash Advances and SBA Loans

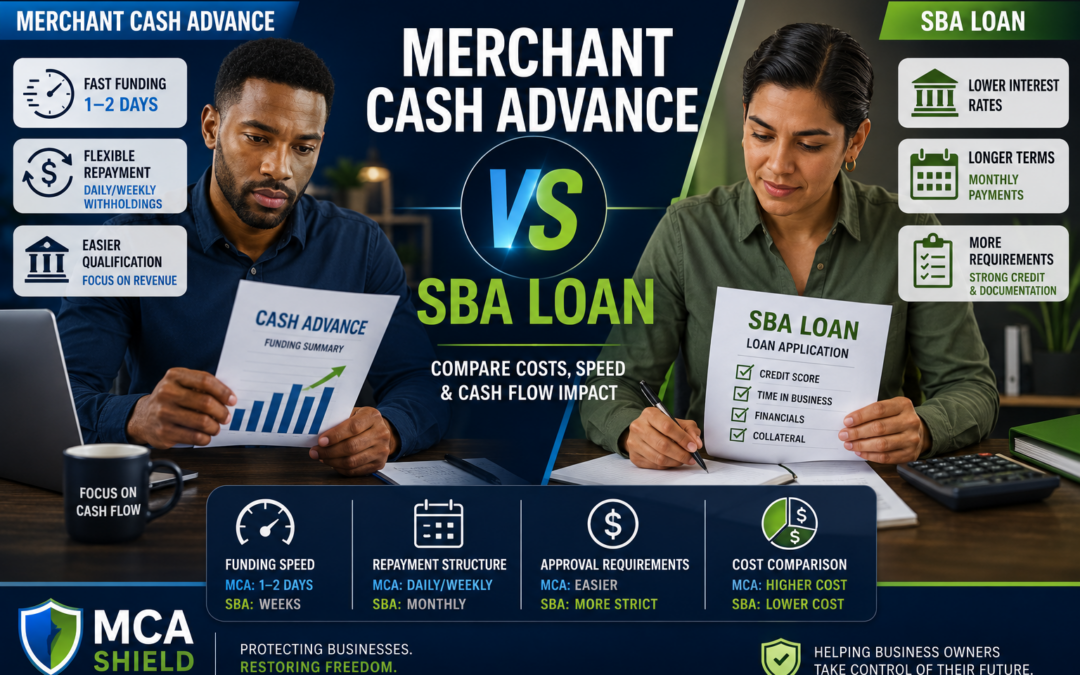

Comparing Approval Requirements

Credit Score Expectations

Merchant Cash Advance: MCA providers often place less emphasis on credit scores and may approve businesses with fair or challenged credit histories.

SBA Loan: SBA lenders typically review personal and business credit carefully and often require stronger credit profiles for approval.

Time in Business Requirements

Merchant Cash Advance: Many MCA companies will consider businesses that have been operating for only a few months.

SBA Loan: SBA lenders generally prefer businesses with an established operating history and proven financial stability.

Revenue and Documentation Requirements

Merchant Cash Advance: MCA approvals often rely heavily on recent revenue and bank activity, with fewer documentation requirements.

SBA Loan: SBA applications usually require detailed financial statements, tax returns, business plans, and supporting documentation during the approval process.

Funding Speed and Access to Capital

One of the primary advantages of a merchant cash advance is speed. Many MCA providers can review applications and deliver funding within one to three business days. This fast approval process often appeals to businesses facing urgent cash flow needs or unexpected expenses.

Typical SBA Loan Approval Timelines

SBA loans generally require a more extensive application and underwriting process. Depending on the lender and loan program, approval and funding can take several weeks or even months. While the process is slower, SBA loans often offer lower costs and longer repayment terms.

When Fast Funding May Be Necessary

Some business situations require immediate access to capital. Unexpected equipment repairs, inventory shortages, seasonal opportunities, or emergency operating expenses may make funding speed a top priority. In these circumstances, business owners often weigh the benefits of rapid MCA funding against the lower long-term costs typically associated with SBA financing.

Repayment Structure and Cash Flow Impact

MCA Daily or Weekly Payments

Most merchant cash advances are repaid through automatic daily or weekly withdrawals from a business bank account. While this structure allows MCA providers to collect payments quickly, the frequent withdrawals can place ongoing pressure on cash flow and reduce the funds available for day-to-day operations.

SBA Loan Monthly Payments

SBA loans typically use a traditional monthly repayment schedule. Because payments are made less frequently and often spread over a longer term, many businesses find SBA loan payments easier to budget for and incorporate into their operating expenses.

How Repayment Affects Working Capital

When comparing a Merchant Cash Advance vs SBA Loan, repayment structure can significantly impact working capital. Daily or weekly MCA payments may reduce the cash available for payroll, inventory, rent, and vendor obligations. Monthly SBA loan payments generally create less immediate cash flow pressure, allowing businesses to retain more working capital between payment due dates.

Comparing Total Costs

Advantages and Disadvantages of Each Option

Potential Benefits of Merchant Cash Advances

Merchant cash advances can provide fast access to capital, often with a simplified approval process and fewer documentation requirements than traditional financing. Businesses with limited credit history or urgent funding needs may find MCA funding easier to obtain when time is a critical factor.

Potential Drawbacks of Merchant Cash Advances

The convenience of MCA funding often comes at a higher cost. Daily or weekly repayment withdrawals can place pressure on cash flow, making it more difficult to cover payroll, inventory, rent, and other operating expenses. Businesses may also face challenges if multiple MCA obligations are taken on at the same time.

Potential Benefits and Limitations of SBA Loans

SBA loans typically offer lower borrowing costs, longer repayment terms, and predictable monthly payments. These features can make them a more affordable financing option for qualified businesses. However, SBA loans generally require stronger credit, more documentation, and a longer approval process, which may not be ideal for businesses that need immediate funding.

When a Merchant Cash Advance May Make Sense

When an SBA Loan May Be the Better Choice

Long-Term Growth and Expansion

An SBA loan may be a better choice for businesses planning long-term growth. Whether funding a new location, purchasing equipment, hiring staff, or expanding operations, SBA financing often provides the larger funding amounts and extended repayment terms needed to support sustainable growth.

Lower-Cost Financing Needs

Businesses focused on minimizing borrowing costs often prefer SBA loans. Lower interest rates and longer repayment schedules can reduce monthly payment obligations and make financing more affordable over time compared to many alternative funding options.

Businesses That Can Wait for Approval

SBA loans typically require a more detailed application and underwriting process. Businesses that are not facing an immediate cash need and can wait several weeks for approval may benefit from the lower costs and more favorable repayment terms that SBA financing often provides.

What Happens When MCA Payments Become Difficult to Manage?

Warning Signs of MCA Payment Pressure

MCA payment pressure often develops gradually before becoming a serious financial problem. Common warning signs include frequent cash flow shortages, difficulty covering payroll or vendor payments, recurring overdrafts, and relying on incoming revenue solely to keep up with daily or weekly withdrawals. Recognizing these signs early may help businesses explore solutions before the situation worsens.

Risks of Taking Additional MCA Funding

When cash flow becomes strained, some business owners consider taking another MCA to cover existing payments. While this may provide temporary relief, it can also increase overall repayment obligations and create additional pressure on future revenue. Multiple advances can make it difficult to manage cash flow and increase the risk of default.

Exploring Relief and Restructuring Options

Businesses struggling with MCA payments may have relief options available. Depending on the situation, solutions may include restructuring existing obligations, negotiating modified payment arrangements, or exploring settlement opportunities. Reviewing all current MCA agreements and evaluating cash flow can help business owners identify strategies that may reduce payment pressure and improve financial stability.

Frequently Asked Questions About Merchant Cash Advances and SBA Loans

Is an SBA Loan Better Than a Merchant Cash Advance?

It depends on the business’s needs. SBA loans are typically less expensive, while MCAs often provide faster access to funding.

Can I Qualify for an SBA Loan After Taking an MCA?

Possibly. Eligibility depends on factors such as credit, revenue, existing debt, and lender requirements.

Why Are MCA Payments More Difficult to Manage?

Daily or weekly withdrawals can create ongoing cash flow pressure and reduce available working capital.

Can MCA Debt Be Restructured or Settled?

In some cases, businesses may be able to pursue restructuring or settlement solutions to reduce payment pressure.

Is a Merchant Cash Advance Considered a Loan?

No. An MCA is generally structured as a purchase of future receivables rather than a traditional loan.

Which Financing Option Is Better for Cash Flow?

SBA loans often provide more predictable monthly payments, while MCA payments can place greater strain on daily cash flow.