MCA factor rates play a major role in determining the true cost of merchant cash advance funding. While many business owners focus on how much funding they receive, the factor rate directly impacts how much they must repay. Even a small increase in the factor rate can significantly raise the total repayment amount and place additional pressure on cash flow.

Unlike traditional business loans that use interest rates, merchant cash advances use factor rates to calculate the total amount owed. Understanding how MCA factor rates work can help business owners evaluate funding offers, compare costs more accurately, and avoid unexpected repayment obligations.

Before accepting any merchant cash advance, it is important to understand how factor rates affect repayment costs and long-term financial stability.

Get an Instant Payment Reduction Quote

What Is an MCA Factor Rate?

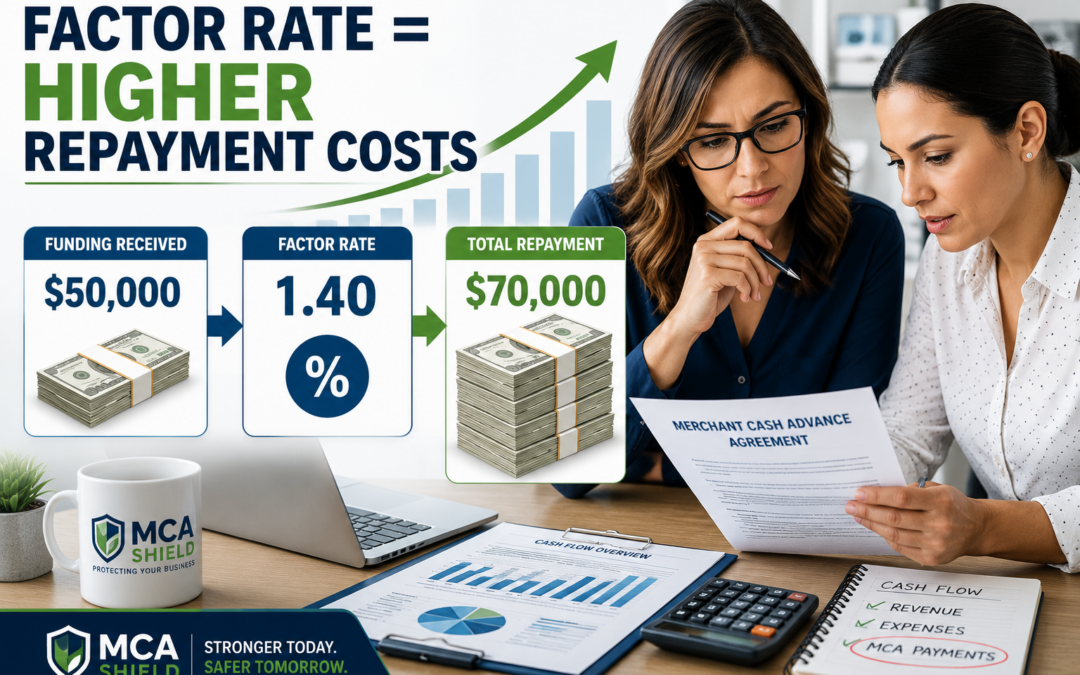

An MCA factor rate is a multiplier that determines the total amount a business must repay on a merchant cash advance. Instead of charging interest over time, MCA providers apply a factor rate to the funding amount at the beginning of the agreement.

For example, if a business receives $50,000 with a factor rate of 1.40, the total repayment amount would be $70,000. The factor rate remains fixed regardless of how quickly the advance is repaid.

How Factor Rates Differ From Traditional Interest Rates

Traditional business loans use annual interest rates that are calculated over time and may decrease as the loan balance is paid down. MCA factor rates work differently. The factor rate is applied to the full funding amount upfront, creating a fixed repayment obligation from the start.

Because factor rates do not account for repayment timing, comparing an MCA factor rate directly to a traditional interest rate can be misleading. In many cases, the effective borrowing cost of an MCA may be significantly higher than it initially appears.

Common MCA Factor Rate Ranges

Most MCA factor rates fall between 1.10 and 1.50, although some agreements may be higher depending on the business’s risk profile, industry, revenue history, and existing debt obligations.

Common examples include:

- 1.10 factor rate: Borrow $50,000, repay $55,000

- 1.25 factor rate: Borrow $50,000, repay $62,500

- 1.40 factor rate: Borrow $50,000, repay $70,000

- 1.50 factor rate: Borrow $50,000, repay $75,000

As the factor rate increases, the total repayment cost rises quickly. Understanding these ranges can help business owners evaluate funding offers and recognize the true cost of MCA financing before signing an agreement.

How MCA Factor Rates Increase Repayment Costs

MCA factor rates directly impact on the total amount a business must repay. While the funding amount may seem attractive initially, the factor rate determines how much additional money is owed beyond the amount received. As the factor rate increases, repayment costs rise quickly, often creating greater pressure on cash flow and profitability.

Understanding how factor rates affect total repayment can help business owners evaluate funding offers more accurately and avoid costly surprises.

Understanding the Total Payback Amount

The total payback amount is calculated by multiplying the funding amount by the factor rate.

For example:

- $50,000 × 1.20 = $60,000 total repayment

- $50,000 × 1.30 = $65,000 total repayment

- $50,000 × 1.40 = $70,000 total repayment

- $50,000 × 1.50 = $75,000 total repayment

Even a small increase in the factor rate can add thousands of dollars to the total repayment obligation.

Why Higher Factor Rates Lead to More Expensive Funding

Many business owners focus on the amount of funding they receive and overlook how the factor rate affects the overall cost. A higher factor rate increases the repayment amount without providing any additional funding.

For example, a business that receives $50,000 at a 1.50 factor rate must repay $20,000 over the amount advanced. Combine this with daily or weekly withdrawals, these higher repayment obligations can reduce working capital, strain cash flow, and make it more difficult to cover payroll, vendors, and operating expenses.

Examples of MCA Factor Rate Calculations

The table below illustrates how repayment costs increase as factor rates rise.

| Funding Amount | Factor Rate | Total Repayment |

|---|---|---|

| $25,000 | 1.20 | $30,000 |

| $25,000 | 1.40 | $35,000 |

| $50,000 | 1.20 | $60,000 |

| $50,000 | 1.40 | $70,000 |

| $75,000 | 1.30 | $97,500 |

| $75,000 | 1.50 | $112,500 |

These examples demonstrate how MCA factor rates can substantially increase repayment costs. Before accepting funding, business owners should calculate the total payback amount and evaluate whether the repayment structure fits their long-term cash flow needs.

The Hidden Cost of Daily and Weekly Payments

While MCA factor rates determine the total repayment amount, the payment structure can create an additional financial burden. Most merchant cash advances require daily or weekly withdrawals directly from a business bank account. Even when sales remain steady, these frequent payments can reduce available working capital and make cash flow more difficult to manage.

For many businesses, the combination of high repayment costs and frequent withdrawals creates challenges that are not immediately obvious when the funding is first received.

How Frequent Withdrawals Affect Cash Flow

Daily and weekly withdrawals remove money from the business on a consistent basis, regardless of upcoming expenses or seasonal fluctuations in revenue. This can leave less cash available for essential operating needs, including:

- Payroll

- Vendor payments

- Inventory purchases

- Rent and utilities

- Marketing and growth initiatives

As payment obligations increase, many businesses find themselves relying on additional financing to maintain normal operations.

Why Repayment Speed Matters

Merchant cash advances are often repaid much faster than traditional business loans. Because payments are collected frequently, the funding may be repaid within several months rather than several years.

This accelerated repayment schedule means businesses must generate enough cash flow to cover both operating expenses and MCA payments at the same time. Even when the total repayment amount remains the same, a faster repayment period can place significantly more pressure on cash flow and reduce financial flexibility.

Understanding both the factor rate and the repayment schedule is essential when evaluating the true cost of MCA financing. In many cases, the frequency of payments can be just as challenging as the repayment amount itself.

Comparing MCA Factor Rates to Traditional Business Loan Costs

Many business owners compare funding offers based on the amount received rather than the total cost of repayment. Because MCA factor rates, repayment schedules, and fee structures differ from traditional loans, understanding the full financial impact is essential before accepting funding.

Factors That Influence MCA Factor Rates

Not every business receives the same MCA factor rate. Funding companies evaluate several factors when determining the level of risk associated with a business. Generally, businesses that demonstrate stronger financial performance and lower risk profiles may qualify for more favorable factor rates, while higher-risk businesses often receive more expensive funding terms.

Understanding what influences MCA factor rates can help business owners better evaluate funding offers and identify potential areas of concern before accepting an advance.

Business Revenue and Risk Profile

Revenue is one of the most important factors to determine MCA pricing. Funding companies often review monthly deposits, average revenue, cash flow consistency, and overall business performance.

Businesses with stable revenue and strong cash flow may be viewed as lower risk and may receive more favorable factor rates. In contrast, businesses experiencing declining sales, frequent overdrafts, or inconsistent deposits may be offered higher factor rates to compensate for the perceived risk.

Industry Type and Time in Business

The industry a business operates in can also influence MCA factor rates. Some industries are considered more volatile or seasonal than others, which may increase the risk for funding providers.

Funding companies often evaluate:

- Industry stability

- Seasonal revenue fluctuations

- Length of time in business

- Historical business performance

Established businesses with a longer operating history may be viewed more favorably than newer companies with limited financial records.

Existing Debt and MCA Stacking

Businesses that already have outstanding financing obligations may face higher factor rates. Existing debt can reduce available cash flow and increase the likelihood of repayment challenges.

MCA stacking—taking multiple merchant cash advances at the same time—often raises additional concerns for funders. Multiple daily or weekly payment obligations can place significant pressure on cash flow, making repayment more difficult and increasing overall risk.

As a result, businesses with stacked MCAs or substantial existing debt may receive higher factor rates, stricter repayment terms, or limited funding options.

Warning Signs of a High-Cost MCA Agreement

Not all merchant cash advances carry the same level of financial risk. Some agreements contain terms that can significantly increase repayment costs and place additional pressure on cash flow. Understanding the warning signs of a high-cost MCA agreement can help business owners avoid unexpected expenses and make more informed funding decisions.

Excessive Repayment Amounts

One of the clearest warning signs is a repayment amount that is substantially higher than the funding received. While MCA factor rates determine the total repayment obligation, some agreements can add tens of thousands of dollars to the amount borrowed.

Before accepting funding, calculate the total payback amount and compare it to the actual funds being received. A large gap between the two may indicate an expensive financing arrangement.

Multiple Fees and Additional Charges

Some MCA agreements include fees beyond the factor rate, increasing the overall cost of funding. These charges may include:

- Origination fees

- Administrative fees

- Processing fees

- Renewal fees

- Default-related charges

Even when individual fees appear small, they can significantly increase the total cost of the advance when combined.

Limited Reconciliation Provisions

Many MCA providers offer reconciliation provisions that allow payments to be adjusted when business revenue declines. However, some agreements place strict limitations on this process or make it difficult to request adjustments.

Limited reconciliation rights can create additional financial pressure during slower business periods because payment obligations may remain unchanged even when revenue decreases. Reviewing these provisions carefully can help business owners better understand the flexibility or lack of flexibility within an MCA agreement.

How Businesses Can Reduce MCA Repayment Pressure

High MCA repayment costs can create significant strain on cash flow, especially when daily or weekly withdrawals begin affecting payroll, vendor payments, and other operating expenses. Fortunately, businesses facing payment pressure may have options. Taking action early often provides more flexibility and may help prevent additional financial challenges.

Reviewing Current MCA Obligations

Start by reviewing all active MCA agreements. Understanding the funding amounts, factor rates, payment schedules, fees, and remaining balances can provide a clearer picture of your total repayment obligations.

Key areas to review include:

- Outstanding balances

- Daily or weekly payment amounts

- Factor rates and total payback amounts

- Additional fees

- Existing MCA stacking

A complete understanding of current obligations is often the first step toward identifying potential solutions.

Exploring MCA Debt Restructuring Options

MCA debt restructuring may help businesses create a more manageable repayment structure. Depending on the circumstances, restructuring can reduce payment pressure, improve cash flow, and provide additional breathing room for daily operations.

Businesses experiencing multiple withdrawals or cash flow disruptions often explore restructuring options before payment challenges become more severe.

Considering MCA Settlement Solutions

For businesses facing significant financial hardship, MCA settlement solutions may be worth evaluating. In some situations, negotiated settlements can help resolve existing obligations for less than the full balance owed.

While every situation is different, exploring settlement opportunities early may provide additional options before defaults, collections, or legal disputes create further complications.

When to Seek Help With Expensive MCA Payments

MCA payments can become a serious problem when they begin interfering with normal business operations. What starts as a manageable funding solution can quickly create cash flow challenges if repayment obligations consume too much of your incoming revenue. Recognizing the warning signs early may help businesses explore solutions before the situation becomes more difficult to resolve.

Signs That Repayment Costs Are Becoming Unmanageable

Businesses often experience several warning signs before MCA payments become overwhelming. Common indicators include:

- Difficulty making payroll

- Frequent overdrafts or negative balances

- Delayed vendor payments

- Declining working capital

- Taking additional MCAs to cover existing obligations

- Using personal funds to support business expenses

If these issues are becoming more common, MCA repayment costs may be placing unsustainable pressure on your business.

Taking Action Before Cash Flow Problems Worsen

Waiting too long to address MCA payment challenges can limit available options. As repayment pressure increases, businesses may face collections, defaults, additional fees, or the need for more expensive financing.

Taking action early often provides greater flexibility. Reviewing your MCA obligations, evaluating restructuring opportunities, and exploring settlement solutions may help create a more sustainable path forward before cash flow problems begin affecting long-term business stability.

MCA payments can become a serious problem when they begin interfering with normal business operations. What starts as a manageable funding solution can quickly create cash flow challenges if repayment obligations consume too much of your incoming revenue. Recognizing the warning signs early may help businesses explore solutions before the situation becomes more difficult to resolve.

Signs That Repayment Costs Are Becoming Unmanageable

Businesses often experience several warning signs before MCA payments become overwhelming. Common indicators include:

- Difficulty making payroll

- Frequent overdrafts or negative balances

- Delayed vendor payments

- Declining working capital

- Taking additional MCAs to cover existing obligations

- Using personal funds to support business expenses

If these issues are becoming more common, MCA repayment costs may be placing unsustainable pressure on your business.

Taking Action Before Cash Flow Problems Worsen

Waiting too long to address MCA payment challenges can limit available options. As repayment pressure increases, businesses may face collections, defaults, additional fees, or the need for more expensive financing.

Taking action early often provides greater flexibility. Reviewing your MCA obligations, evaluating restructuring opportunities, and exploring settlement solutions may help create a more sustainable path forward before cash flow problems begin affecting long-term business stability.

Frequently Asked Questions About MCA Factor Rates

Taking Action Before MCA Repayment Costs Get Worse

MCA factor rates directly impact how much a business ultimately repays. While the funding amount may provide short-term working capital, higher factor rates can significantly increase repayment costs and place additional pressure on cash flow through daily or weekly withdrawals.

Before accepting any merchant cash advance, it is important to understand the total repayment obligation, review all fees and contract terms, and evaluate how the payment structure may affect your business over time. A clear understanding of the true cost of funding can help prevent unexpected financial strain and support more informed decision-making.

If MCA payments are creating cash flow challenges or becoming difficult to manage, help may be available. Schedule a free consultation with MCA Shield to review your current MCA obligations, explore restructuring or settlement options, and identify potential strategies for reducing payment pressure and improving financial stability.