A Merchant Cash Advance and a traditional business loan may both provide funding, but they can affect your business very differently. Traditional loans typically offer predictable payments and longer repayment terms, while MCAs often rely on daily or weekly withdrawals that can quickly strain cash flow. Understanding these differences before signing an agreement is critical. The right financing choice can support growth and stability, while the wrong one can create financial pressure that becomes difficult to overcome.

Get an Instant Payment Reduction Quote

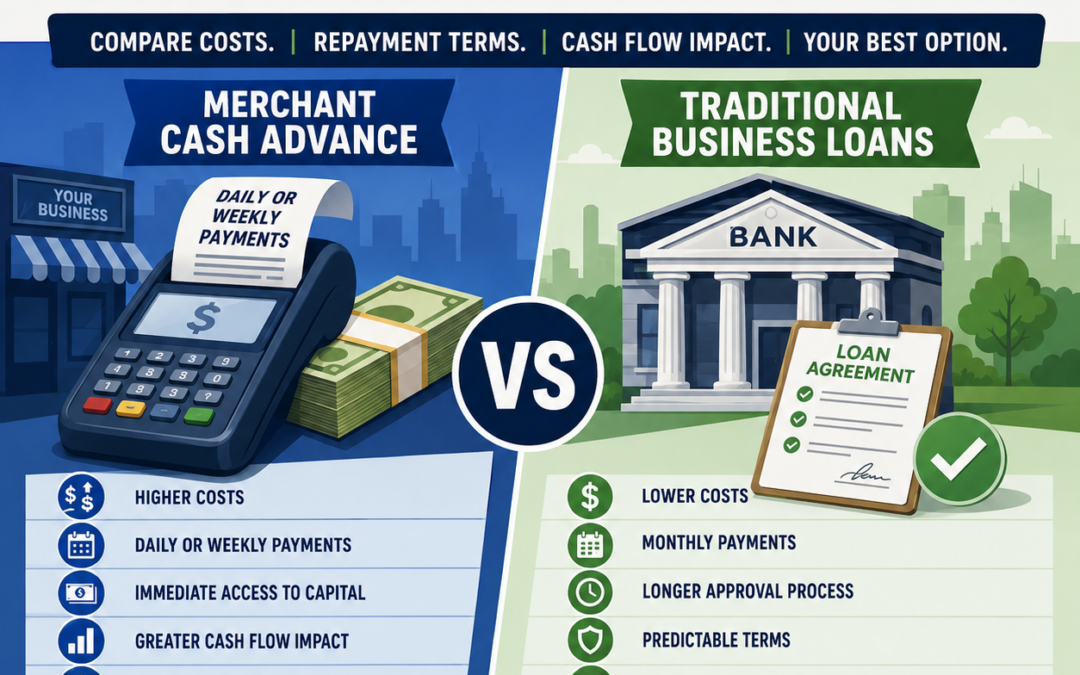

What Is the Difference Between a Merchant Cash Advance and a Traditional Business Loan?

At a high level, both a Merchant Cash Advance (MCA) and a traditional business loan provide access to capital. The biggest difference lies in how the money is repaid. Traditional business loans typically offer fixed monthly payments and a defined repayment schedule. MCAs often use daily or weekly withdrawals tied to business revenue, which can place more pressure on cash flow.

Key differences often include:

• Repayment Structure – Loans usually have monthly payments, while MCAs often require daily or weekly withdrawals.

• Approval Requirements – MCAs generally offer faster approvals and funding.

• Cost Structure – Loans typically use interest rates, while MCAs often use factor rates.

• Cash Flow Impact – MCA payments can fluctuate and may affect working capital more quickly.

Understanding these differences is critical before choosing a financing option. What appears to be the fastest solution today may not always be the most affordable or sustainable choice over the long term.

How Repayment Structures Differ Between MCAs and Business Loans

One of the biggest differences between a Merchant Cash Advance and a traditional business loan is the repayment structure. Traditional loans usually require fixed monthly payments over a set period. This makes budgeting and cash flow planning more predictable. MCAs often collect payments through daily or weekly withdrawals, which can place ongoing pressure on operating capital.

| Feature | Merchant Cash Advance | Traditional Business Loan |

|---|---|---|

| Payment Frequency | Daily or Weekly | Monthly |

| Payment Amount | May fluctuate based on terms | Typically fixed |

| Cash Flow Impact | Often higher | Usually more predictable |

| Repayment Period | Often shorter | Often longer |

| Budgeting Ease | Can be challenging | Generally easier |

The repayment structure matters more than many business owners realize. A payment that seems manageable at first can become difficult when withdrawals occur every day. Understanding how repayment works before accepting funding can help you choose the option that best supports your business’s long-term financial health.

Which Option Costs More: MCA vs Traditional Business Loan?

In many cases, Merchant Cash Advances cost significantly more than traditional business loans. While business loans typically use interest rates and longer repayment terms, MCAs often use factor rates and shorter repayment periods. As a result, the total amount repaid can be much higher than many business owners initially expect.

The challenge is not just the cost itself. Daily or weekly withdrawals can make expensive funding feel even more burdensome. What starts as a quick source of capital can quickly become a strain on cash flow, especially during slower sales periods. Before accepting any financing offer, business owners should carefully compare the total repayment amount, payment structure, and long-term impact on their business.

The Impact on Cash Flow: Merchant Cash Advances vs Business Loans

Cash flow is often where the difference between a Merchant Cash Advance and a traditional business loan becomes most noticeable. Traditional loans generally offer fixed monthly payments, which makes budgeting easier and more predictable. MCAs often rely on daily or weekly withdrawals, reducing available cash on a much more frequent basis.

| Cash Flow Factor | Merchant Cash Advance | Traditional Business Loan |

|---|---|---|

| Payment Frequency | Daily or Weekly | Monthly |

| Budget Predictability | Lower | Higher |

| Impact on Working Capital | Often Greater | Usually Lower |

| Cash Flow Flexibility | More Limited | More Flexible |

Even profitable businesses can experience cash flow challenges when frequent withdrawals begin consuming too much revenue. While every situation is different, business owners should consider how repayment frequency affects payroll, inventory purchases, rent, and other operating expenses. The financing option that looks fastest upfront is not always the one that best supports long-term financial stability.

When a Merchant Cash Advance May Make Sense

While Merchant Cash Advances often receive criticism for their cost, there are situations where they may make sense. Businesses that need funding quickly and cannot qualify for traditional financing sometimes turn to MCAs as a short-term solution. Fast approval times and minimal documentation requirements can make them attractive when immediate access to capital is critical.

For example, a business may use an MCA to cover an urgent expense, purchase inventory for a major opportunity, or bridge a temporary cash flow gap. In these situations, the speed of funding may outweigh the higher cost. The key is having a clear plan for repayment before accepting the advance.

An MCA works best when it serves as a temporary tool rather than a long-term financing strategy. Business owners should carefully weigh the benefits against the repayment structure and total cost. What solves a short-term problem should not create a long-term financial burden.

Warning Signs Your MCA Payments Are Becoming Unmanageable

MCA payments often become unmanageable gradually rather than all at once. What starts as a helpful source of funding can begin creating serious cash flow pressure as daily or weekly withdrawals consume more of your revenue. The earlier you recognize the warning signs, the easier it may be to address the problem before it escalates.

Common warning signs include:

• Struggling to cover payroll or operating expenses

• Frequently overdrawing business accounts

• Falling behind on vendor payments

• Using one advance to pay another

• Experiencing constant cash flow shortages

• Missing or delaying important business obligations

One of the biggest red flags is taking on additional MCA debt just to keep up with existing payments. This can create a cycle that becomes increasingly difficult to escape. If you recognize several of these warning signs, it may be time to explore restructuring, consolidation, or other mca relief options before the situation becomes more severe.

What Are Your Options If MCA Payments Become Too Expensive?

If MCA payments have become too expensive, you are not necessarily out of options. Many business owners face cash flow challenges after taking on one or more advances, especially when daily or weekly withdrawals begin consuming too much revenue. Taking action early can often create more opportunities for relief.

Potential solutions may include:

• MCA Debt Consolidation

• Debt Restructuring Programs

• Negotiated Settlements

• Payment Modifications

• Cash Flow Improvement Strategies

The most important step is addressing the problem before it gets worse. Waiting too long can increase financial pressure and limit your flexibility. By exploring available options early, many businesses can reduce payment stress, regain control of cash flow, and create a more sustainable path forward.

Success Stories from Our Clients

“Thanks to mcashield.com, we reduced our daily payments significantly and saved our business from financial distress.”

John D., Restaurant Owner

“The consolidation process was seamless, and now we can focus on growing our business instead of worrying about multiple payments.”

Emily R., Retail Store Manager

“I was skeptical at first, but mcashield.com delivered on their promise. Our cash flow has improved dramatically.”

Michael T., Small Business Owner

Get a Free MCA Consolidation Quote

Unlock the potential for a brighter financial future by exploring our MCA consolidation options, designed to transform your existing cash flow challenges into manageable solutions without the burden of new loans or credit checks. Picture this: a streamlined payment process that empowers you to regain control of your business while alleviating the stress of juggling multiple lenders. By consolidating your merchant cash advances now, you can simplify your financial landscape, ensure timely payments to vendors, and protect your valuable resources from unpredictable cash flow pitfalls. Take the proactive step towards efficiency and peace of mind—your business deserves this chance to thrive.