Merchant Cash Advance Contracts can contain complex terms that many business owners do not fully understand until payment pressure begins affecting cash flow. While merchant cash advances can provide fast access to working capital, the agreements often include provisions related to repayment, ACH withdrawals, default, personal guarantees, and collection rights that may have significant financial consequences.

Unlike traditional business loans, merchant cash advance agreements are structured as purchases of future receivables. As a result, the language used in these contracts can be confusing for business owners who are unfamiliar with factor rates, holdback percentages, reconciliation clauses, and other industry-specific terms.

One common misconception is that all merchant cash advance contracts work the same way. In reality, contract terms can vary substantially from one funding company to another. Some agreements contain flexible repayment provisions, while others may include aggressive default language or restrictions that can create challenges if business revenue declines.

Understanding a merchant cash advance contract before signing is one of the most important steps a business owner can take. By reviewing the key provisions carefully, businesses can better evaluate the true cost of the funding, identify potential risks, and make more informed financial decisions.

Get an Instant Payment Reduction Quote

What Is a Merchant Cash Advance Contract?

A Merchant Cash Advance Contract is the legal agreement that outlines the terms of a merchant cash advance transaction. The contract explains how much funding the business will receive, how repayment will occur, what obligations both parties must follow, and what happens if the agreement is not fulfilled.

Before accepting funding, it is important to understand the terms contained in the contract. Many business owners focus on the amount being advanced, but the agreement often contains provisions that affect repayment, collections, default, and future financing opportunities.

How MCA Contracts Differ From Traditional Loan Agreements

One of the biggest differences between a merchant cash advance and a traditional business loan is the structure of the transaction. A business loan involves borrowing money and repaying it with interest over a set period. A merchant cash advance, by contrast, is structured as the purchase of a portion of the business’s future receivables.

Because the transaction is not presented as a conventional loan, Merchant Cash Advance Contracts often use different terminology. Instead of interest rates, agreements may reference factor rates. Instead of monthly loan payments, contracts may discuss holdbacks, ACH withdrawals, or purchased receivables.

This distinction is important because the structure of the agreement can affect repayment obligations, default provisions, and the overall cost of the funding.

The Purpose of an MCA Agreement

The primary purpose of a Merchant Cash Advance Contract is to define the rights and responsibilities of both the business and the funding company. The agreement establishes how much funding will be provided, how payments will be collected, and what actions each party must take throughout the relationship.

Merchant Cash Advance Contracts also contain payment and collection provisions. These sections typically explain how funds will be withdrawn, when payments are due, what constitutes a default, and what remedies may be available if the agreement is breached.

Carefully reviewing these provisions before signing can help business owners understand their obligations and avoid unexpected issues later in the repayment process.

Key Terms Found in Most Merchant Cash Advance Contracts

Understanding the terminology used in Merchant Cash Advance Contracts can help business owners evaluate the true cost of funding and avoid surprises. The following terms appear in many MCA agreements and deserve careful review before signing.

Purchase Price

The purchase price is the amount of money the funding company provides to the business. This is the amount deposited into your account after the agreement is finalized.

Purchased Amount

The purchased amount is the total future receivables that the MCA company is buying. This amount is usually higher than the purchase price and represents the total amount that must be collected under the agreement.

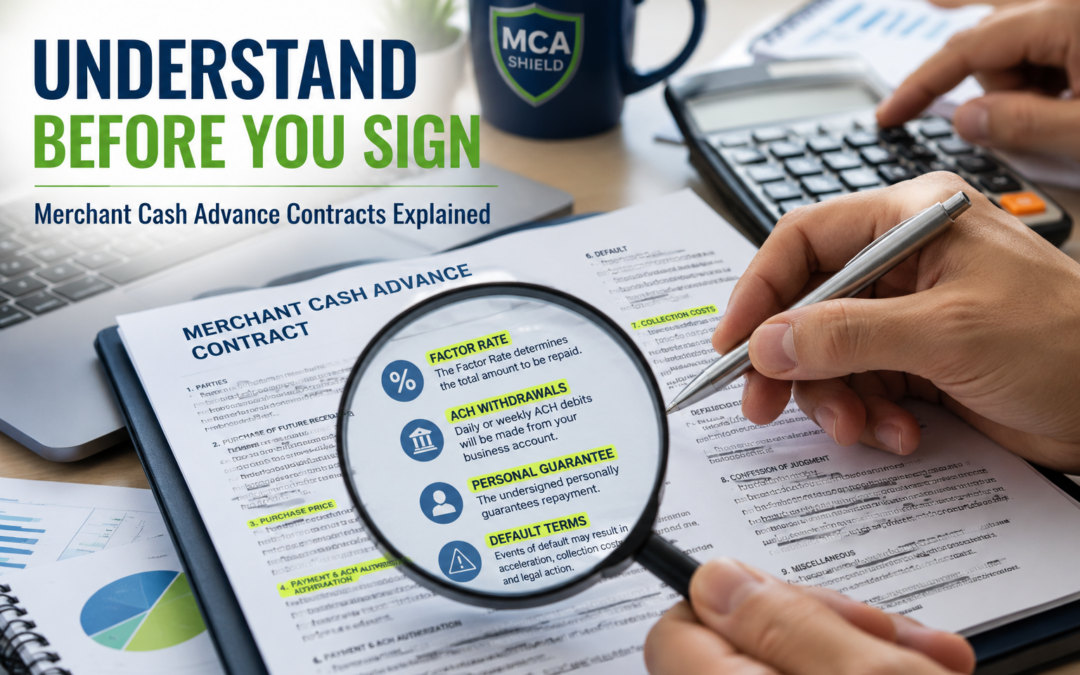

Factor Rate

A factor rate determines the total repayment amount. Unlike an interest rate, the factor rate is multiplied by the funding amount to calculate the total amount owed.

Total Repayment

The total repayment is calculated using the factor rate. For example, a $50,000 advance with a 1.40 factor rate results in a total repayment obligation of $70,000.

Holdback Percentage

The holdback percentage is the portion of daily or weekly revenue that is applied toward repayment. This percentage directly affects the size of ongoing withdrawals.

ACH Withdrawals

Many Merchant Cash Advance Contracts collect payments through daily or weekly ACH withdrawals. These automatic deductions are typically based on estimated business revenue.

Reconciliation Clause

A reconciliation clause may allow payment adjustments when revenue increases or decreases. Not all MCA agreements contain meaningful reconciliation provisions, making this section important to review carefully.

Estimated Repayment Period

Many Merchant Cash Advance Contracts do not have a fixed repayment term. Instead, contracts provide an estimated repayment period based on projected sales and revenue performance.

Understanding ACH Withdrawal Provisions

Most Merchant Cash Advance Contracts rely on Automated Clearing House (ACH) withdrawals to collect payments. These withdrawals are typically taken directly from the business bank account on a daily or weekly basis. Understanding how ACH payments work can help business owners avoid unexpected cash flow issues and identify potential risks before signing an agreement.

How MCA Companies Collect Payments

Most MCA companies collect payments through automatic ACH withdrawals from the business bank account. Depending on the agreement, withdrawals may occur daily or weekly.

The payment amount is often based on estimated revenue and the terms outlined in the Merchant Cash Advance Contract. Because these withdrawals occur automatically, they can significantly impact available cash flow.

What Happens if ACH Payments Fail?

Failed ACH withdrawals can create additional financial pressure for a business. If there are insufficient funds in the account, the business may incur NSF fees, bank overdraft fees, or both.

In many Merchant Cash Advance Contracts, repeated failed payments can also trigger a default. Once a default occurs, collection efforts may escalate, and additional remedies outlined in the agreement may become available to the funding company.

Can ACH Payments Be Modified?

Some Merchant Cash Advance Contracts contain provisions that allow payment adjustments when business revenue changes significantly. These provisions are commonly referred to as reconciliation clauses.

However, not all agreements provide meaningful adjustment rights. Before signing, business owners should carefully review the contract language to determine whether payment modifications are available and what requirements must be met to request an adjustment.

Personal Guarantees in Merchant Cash Advance Contracts

Many Merchant Cash Advance Contracts include a personal guarantee. While business owners often focus on funding amounts and payment terms, understanding personal guarantee provisions is equally important. These clauses may affect an owner’s financial obligations if problems arise during repayment.

What Is a Personal Guarantee?

A personal guarantee is a contractual provision that may hold a business owner personally responsible for certain obligations under the agreement. By signing the contract, the owner may agree to specific responsibilities that extend beyond the business itself.

The exact language and scope of a personal guarantee can vary between Merchant Cash Advance Contracts. For this reason, business owners should carefully review the agreement before signing.

When Personal Liability May Become an Issue

Personal liability concerns often arise when a business experiences financial difficulties or is unable to meet its contractual obligations. Depending on the terms of the agreement, disputes regarding repayment, alleged defaults, or other contract-related issues may increase the importance of the personal guarantee provision.

Because every contract is different, business owners should understand when personal obligations may become relevant and what rights the funding company may have under the agreement.

Common Misunderstandings About Personal Guarantees

One common misconception is that all personal guarantees are identical. In reality, the language, scope, and enforcement provisions can vary significantly between agreements.

Another misunderstanding is that business owners automatically understand the full impact of the guarantee simply by signing the contract. Many Merchant Cash Advance Contracts contain complex legal language that may not be obvious during the funding process.

Before signing any agreement, it is important to review the personal guarantee provisions carefully and understand how they may affect your rights and obligations.

Default Clauses Every Business Owner Should Review

Default provisions are among the most important sections of any Merchant Cash Advance Contract. These clauses define what actions may place a business in default and what rights the funding company may have if a default occurs. Understanding these provisions before signing can help business owners avoid unexpected consequences.

What Constitutes a Default?

A default occurs when a business fails to meet certain obligations outlined in the Merchant Cash Advance Contract. While missed payments are a common cause of default, contracts often contain additional provisions that can trigger a default even when payments are current.

Because default definitions vary between agreements, business owners should carefully review the contract language and understand all potential default events.

Common Default Triggers

Missed Payments

Failed ACH withdrawals, insufficient funds, or repeated payment issues are common default triggers in many MCA agreements.

Bank Account Changes

Some contracts require businesses to maintain a specific bank account for payment collection. Unauthorized account changes may trigger a default under certain agreements.

Additional Financing or MCA Stacking

Many Merchant Cash Advance Contracts restrict additional financing. Taking on new funding without approval may violate contract terms and create default issues.

Business Closure

Closing the business or ceasing operations may trigger default provisions because the funding company relies on future business revenue for repayment.

What Happens After Default?

Collections

After a default, collection efforts often become more aggressive. Businesses may receive increased communication regarding the outstanding obligation.

Legal Action

Depending on the contract terms and circumstances, the funding company may pursue legal remedies available under the agreement.

Increased Payment Pressure

Defaults can create additional financial strain through collection activity, fees, legal expenses, and reduced flexibility in resolving the obligation.

Because default provisions can significantly affect a business, reviewing these clauses before signing a Merchant Cash Advance Contract is essential.

UCC Liens and Security Interests in MCA Agreements

Many Merchant Cash Advance Contracts include provisions related to UCC filings and security interests. While these filings do not always affect daily business operations, they can create challenges when a business seeks additional financing. Understanding how UCC liens work can help business owners avoid surprises and make more informed funding decisions.

What Is a UCC Filing?

A UCC filing, often called a UCC-1 financing statement, is a public notice to establish a claimed interest in certain business assets or receivables. MCA companies may file a UCC lien to protect their interest in the agreement.

A UCC filing does not necessarily mean the business has done anything wrong. In many cases, it is a standard part of the funding process.

How UCC Liens Can Affect Future Financing

UCC liens can sometimes create obstacles when a business applies for new financing. Lenders and financing companies often review existing UCC filings as part of their approval process.

An active UCC lien may limit financing options, delay approvals, or require additional review before new funding can be obtained. For businesses seeking loans, lines of credit, or equipment financing, existing liens can become an important consideration.

Removing or Resolving Existing Liens

Once an MCA obligation has been satisfied, the related UCC filing may be eligible for termination or release. However, the process can vary depending on the agreement and the filing party.

If a business believes a UCC lien should no longer be active, it may be beneficial to verify the filing status and determine whether additional action is required. Addressing outdated or unresolved liens can help improve access to future financing opportunities.

Confession of Judgment and Other Collection Provisions

A Confession of Judgment (COJ) is a legal provision used in some commercial financing agreements. The specific language and enforceability of a Confession of Judgment can vary based on the contract and applicable laws.

Because of the potential legal implications, business owners should carefully review any agreement that references a Confession of Judgment and understand how it may affect their rights.

Collection Rights MCA Companies May Include

Merchant Cash Advance Contracts may contain various collection provisions that outline the funding company’s rights if a default occurs. Common examples include:

Collection Efforts

The agreement may authorize the funding company to pursue collection activity if contractual obligations are not met.

UCC Filings

Some MCA companies file UCC liens to protect their interest in the purchased receivables.

Legal Remedies

Contracts often describe the legal remedies that may be available if a dispute or default occurs.

Recovery of Costs

Certain agreements may allow the recovery of collection costs, legal expenses, or other fees under specific circumstances.

Why Collection Language Deserves Careful Review

Many business owners focus on funding amounts and payment terms while overlooking collection provisions. However, these sections often define what happens if business revenue declines or repayment challenges develop.

Carefully reviewing collection language can help identify potential risks, clarify obligations, and provide a better understanding of the consequences that may follow a default. Before signing any Merchant Cash Advance Contract, it is important to understand both the funding benefits and the collection provisions contained in the agreement.

Warning Signs of a High-Risk Merchant Cash Advance Contract

Not all Merchant Cash Advance Contracts carry the same level of risk. Some agreements contain provisions that can increase repayment pressure, limit flexibility, or create additional financial challenges if business conditions change. Before signing, business owners should carefully review the contract for potential warning signs.

Excessive Factor Rates

The factor rate directly affects the total amount that must be repaid. Higher factor rates increase the overall cost of the advance and can significantly reduce available cash flow over time.

Business owners should understand the total repayment obligation and compare funding options before accepting an agreement.

Aggressive Default Language

Some Merchant Cash Advance Contracts contain broad default provisions that extend beyond missed payments. Certain agreements may define default events in ways that create additional risk for the business.

Carefully reviewing default language can help identify potential obligations and consequences before problems arise.

Limited Reconciliation Rights

Reconciliation provisions may allow payment adjustments when business revenue changes. However, some contracts offer limited reconciliation rights or contain restrictions that make adjustments difficult to obtain.

Understanding how reconciliation works can be important if revenue fluctuates during the repayment period.

Multiple Fees and Hidden Costs

In addition to repayment obligations, some agreements may include administrative fees, collection costs, legal expenses, or other charges that increase the overall cost of the funding.

Business owners should review all fees carefully and understand how they may affect the total financial obligation.

Restrictions on Additional Financing

Some Merchant Cash Advance Contracts restrict a business’s ability to obtain additional financing while the agreement remains active. These restrictions may affect future funding opportunities or create challenges when additional working capital is needed.

Reviewing these provisions before signing can help avoid financing limitations later.

Quick Contract Review Checklist

Before signing a Merchant Cash Advance Contract, look for:

⚠️ High factor rates

⚠️ Broad default provisions

⚠️ Limited reconciliation rights

⚠️ Multiple fees and added costs

⚠️ Restrictions on future financing

Identifying these warning signs early can help business owners make more informed funding decisions and avoid unnecessary financial pressure.

What to Do Before Signing a Merchant Cash Advance Contract

A Merchant Cash Advance Contract can affect your business long after the funding is received. Before signing any agreement, it is important to understand the repayment terms, identify potential risks, and evaluate whether the funding aligns with your business’s financial goals. Taking time to review the contract carefully may help prevent costly surprises later.

Review All Repayment Obligations

Before signing, make sure you understand the total repayment amount, factor rate, holdback percentage, and payment schedule. Review how payments will be collected and determine how much funding will ultimately be repaid over the life of the agreement.

Understanding the full repayment obligation can help you accurately evaluate the cost of the funding.

Understand Default and Collection Provisions

Default and collection clauses often have a significant impact on a Merchant Cash Advance Contract. Review what actions may trigger a default and what collection rights the funding company may have if repayment issues occur.

Pay close attention to provisions related to ACH withdrawals, UCC filings, collection costs, and other remedies outlined in the agreement.

Evaluate Cash Flow Impact

Even if the funding amount appears attractive, the repayment structure must fit your business’s cash flow. Consider how daily or weekly withdrawals may affect payroll, vendor payments, inventory purchases, and other operating expenses.

A funding solution that creates ongoing cash flow strain may lead to additional financial challenges in the future.

Compare Alternative Financing Options

Before committing to a Merchant Cash Advance Contract, compare other financing solutions that may be available. Depending on your situation, alternatives such as business loans, lines of credit, equipment financing, or MCA restructuring options may provide more flexibility.

Evaluating multiple options can help ensure you select the solution that best supports your long-term business goals.

Pre-Signing Checklist

Before signing a Merchant Cash Advance Contract, ask yourself:

✔️ Do I understand the total repayment amount?

✔️ Have I reviewed all default provisions?

✔️ Can my cash flow support the payment schedule?

✔️ Do I understand the collection provisions?

✔️ Have I compared alternative financing options?

Taking these steps before signing can help you make a more informed decision and reduce the risk of future financial pressure.

What If You Already Signed an MCA Contract?

The first step is understanding exactly what obligations remain under your Merchant Cash Advance Contract. Review the agreement carefully and identify:

- Remaining balance obligations

- Payment frequency and withdrawal amounts

- Factor rate and total repayment terms

- Default provisions

- Collection rights and UCC filings

Having a clear picture of your current obligations can help you evaluate the most appropriate path forward.

Options for Businesses Struggling With Payments

If MCA payments have become difficult to manage, several potential solutions may be available depending on your circumstances.

Restructuring

MCA restructuring may help reduce payment pressure by modifying repayment terms and creating a more manageable payment arrangement. The goal is often to improve cash flow while allowing the business to continue operating.

Settlement Programs

In some situations, settlement opportunities may be available. A negotiated settlement may resolve MCA obligations for less than the full amount claimed, although results vary based on the facts of each case.

Debt Relief Solutions

Businesses facing multiple advances, significant cash flow challenges, or collection pressure may benefit from exploring broader MCA debt relief strategies. These solutions are often designed to create a more sustainable path forward while addressing existing obligations.

When to Seek Professional Guidance

The earlier repayment problems are addressed, the more options may be available. Waiting until defaults, collections, or legal disputes occur can make resolving MCA debt more difficult.

If daily withdrawals are affecting payroll, vendor payments, inventory purchases, or normal operations, it may be beneficial to seek professional guidance. An experienced MCA debt relief professional can review your situation, explain available options, and help you determine the most appropriate strategy for your business.

Signs It May Be Time to Explore Help

⚠️ Multiple MCA balances

⚠️ Frequent overdrafts

⚠️ Difficulty making payroll

⚠️ Vendor payment delays

⚠️ Reliance on new advances to cover existing obligations

⚠️ Ongoing collection pressure

Recognizing these warning signs early may help prevent larger financial challenges and provide more flexibility when evaluating available solutions.

Taking Action Before MCA Contract Terms Create Financial Pressure

Merchant Cash Advance Contracts contain important provisions that can affect your business’s cash flow, financing options, and financial flexibility. Understanding these terms before signing can help you identify potential risks, evaluate the true cost of funding, and avoid unexpected challenges later.

Whether you are reviewing a new agreement or already managing an existing MCA, taking the time to understand repayment obligations, default provisions, collection rights, and other key contract terms can help you make more informed business decisions.

If MCA payments are becoming difficult to manage, do not wait until cash flow problems, collections, or defaults create additional pressure. In many cases, addressing the situation early provides more options and greater flexibility.

Schedule a free consultation with MCA Shield to review your MCA contract, evaluate your current obligations, and explore potential restructuring, settlement, or debt relief solutions. Our team can help you better understand your options and identify a path that supports your business’s long-term success.