Can MCA Companies Take Money Without Warning? This is a common question among business owners who rely on merchant cash advances for working capital. Unexpected withdrawals from a business bank account can create immediate cash flow challenges, making it difficult to cover payroll, vendor payments, rent, and other essential operating expenses.

Most MCA agreements authorize automatic ACH withdrawals, but many business owners are unsure when payments can be deducted or what happens if account balances are lower than expected. Understanding how MCA withdrawals work, when funds may be collected, and what options are available when payments become difficult to manage can help businesses avoid larger financial problems. By recognizing warning signs early, business owners may be able to protect cash flow and explore solutions before the situation becomes more serious.

Get an Instant Payment Reduction Quote

How MCA Companies Typically Collect Payments

Merchant cash advance providers generally collect payments through automatic withdrawals from a business bank account. Unlike traditional loans, which often require monthly payments, MCA companies typically use ACH withdrawals on a daily or weekly basis. These automatic debits are designed to provide consistent repayment and are usually established when the funding agreement is signed.

Understanding how these payment systems work can help business owners better manage cash flow and avoid unexpected account shortages. Reviewing the terms of an MCA agreement is often the first step toward understanding when withdrawals may occur and how repayment obligations can affect day-to-day operations.

Understanding ACH Withdrawals and Automatic Debits

Most MCA companies use Automated Clearing House (ACH) transfers to collect payments directly from a business checking account. Once the agreement is in place, withdrawals are typically processed automatically according to the payment schedule outlined in the contract.

Because these withdrawals occur electronically, funds can leave an account without a separate reminder or approval each time a payment is due. For businesses with fluctuating revenue, frequent ACH withdrawals can sometimes create cash flow challenges if account balances are not closely monitored.

What Authorization Business Owners Agree To

When accepting a merchant cash advance, business owners generally authorize the MCA company to withdraw payments directly from a designated bank account. This authorization is typically included in the funding agreement and may remain in effect throughout the repayment period.

Many business owners focus primarily on the funding amount and repayment cost while overlooking the details of the withdrawal authorization. Reviewing these provisions carefully can help clarify when payments may be collected and what rights the MCA company may have under the agreement.

Daily vs. Weekly MCA Payment Structures

MCA repayment schedules commonly involve either daily or weekly withdrawals. Daily payment structures involve smaller, more frequent deductions, while weekly payments combine those obligations into larger withdrawals that occur less often.

The payment structure can have a significant impact on business cash flow. Daily withdrawals may create ongoing pressure on available working capital, while weekly withdrawals result in larger fluctuations. Understanding the repayment schedule can help business owners plan for expenses and identify potential cash flow concerns before they become more serious.

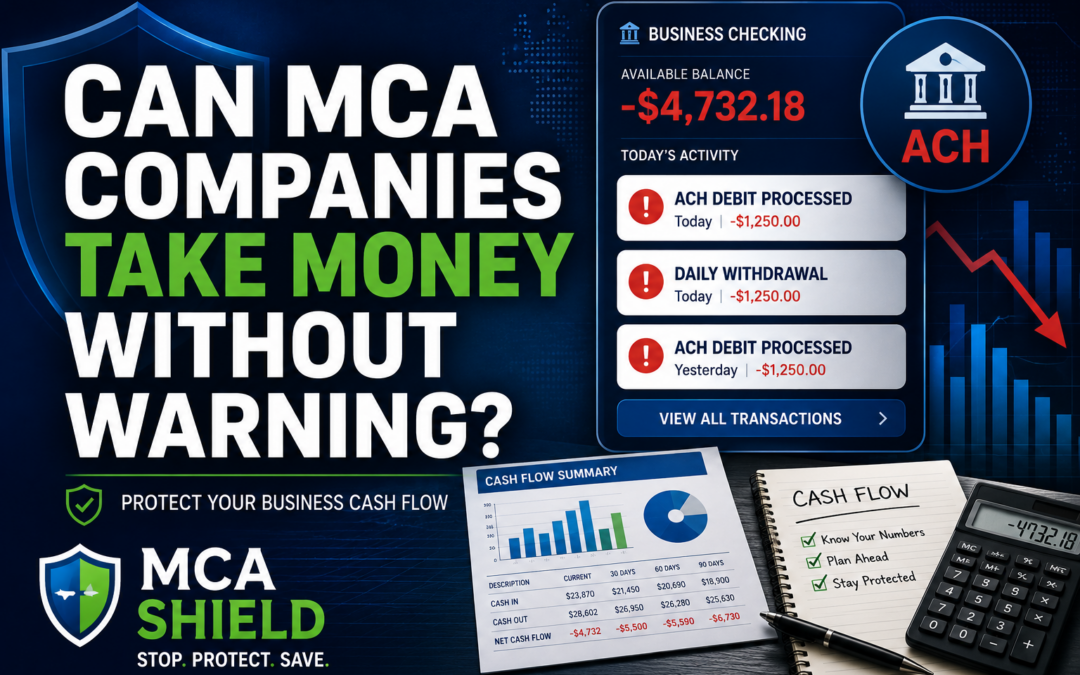

Can MCA Companies Withdraw Funds Without Advance Notice?

Many business owners wonder whether MCA companies can withdraw funds without advance notice. Most MCA companies collect payments based on the terms established when the funding agreement is signed. After ACH authorization is provided, withdrawals are typically processed automatically from the business bank account, and business owners may not receive a separate reminder before each scheduled payment.

While these withdrawals are often expected under the agreement, businesses may still feel surprised when funds leave their account during periods of low cash flow. Understanding when withdrawals usually occur and what situations can lead to unexpected payment activity can help business owners avoid disruptions and better manage their finances.

When Scheduled Withdrawals Usually Occur

Most MCA providers establish a fixed repayment schedule when funding is issued. Depending on the agreement, ACH withdrawals may occur daily, weekly, or on another predetermined schedule. Payments are often deducted automatically from the business bank account without requiring additional approval each time.

Because the withdrawal schedule is typically outlined in the contract, many MCA companies do not provide advance notice before each payment. Business owners are generally expected to maintain sufficient funds in the designated account in agreement with the repayment terms.

Situations That May Lead to Unexpected Withdrawals

Several situations can make MCA withdrawals feel unexpected, even when they are technically authorized. Business owners may overlook payment schedules, experience sudden revenue declines, or lose track of multiple MCA obligations being withdrawn from the same account.

In some cases, payment amounts may change if the agreement includes provisions tied to business revenue or reconciliation adjustments. Multiple merchant cash advances, commonly known as loan stacking, can also make it more difficult to anticipate when funds will be withdrawn and how those withdrawals will affect available cash flow.

Why Business Owners Sometimes Feel Caught Off Guard

Business owners often feel caught off guard when MCA withdrawals coincide with payroll, vendor payments, rent obligations, or other critical expenses. Even if the withdrawal was scheduled, the timing can create immediate financial pressure when cash reserves are limited.

Unexpected cash flow shortages may become more common as repayment obligations increase or business revenue becomes less predictable. When MCA withdrawals begin interfering with normal operations, it may be a sign that the current repayment structure is no longer sustainable and that MCA relief options should be explored before larger financial challenges develop.

What Happens When MCA Payments Exceed Available Cash Flow

Merchant cash advance payments can become difficult to manage when daily or weekly withdrawals consume too much of a business’s available cash flow. What may have seemed like an affordable payment structure initially can create significant financial pressure as revenue fluctuates, expenses increase, or multiple MCA obligations accumulate.

When MCA payments exceed available cash flow, business owners often face difficult decisions about which expenses to prioritize. As cash reserves shrink, it can become harder to maintain normal operations, cover essential costs, and keep pace with ongoing repayment obligations.

Overdraft Fees and Returned Payments

One of the most immediate consequences of cash flow shortages is the risk of overdraft fees and returned ACH payments. If sufficient funds are not available when an MCA withdrawal is processed, the bank may reject the transaction or charge additional fees.

Repeated overdrafts and returned payments can quickly increase financial strain. These issues may also trigger collection activity or additional pressure from MCA providers seeking repayment.

Impact on Payroll, Vendors, and Operating Expenses

When MCA withdrawals consume a large portion of incoming revenue, businesses may struggle to cover other important expenses. Payroll, inventory purchases, vendor payments, rent, utilities, and other operating costs often compete for the same limited cash flow.

As financial pressure grows, delayed payments can disrupt business operations and damage relationships with employees, suppliers, and service providers. Maintaining adequate working capital becomes increasingly difficult when repayment obligations absorb too much of the company’s available funds.

The Risk of Falling Behind on MCA Obligations

Businesses facing ongoing cash flow challenges may increasingly struggle to stay current with MCA payments. Missed or returned withdrawals can create additional stress as repayment obligations continue to accumulate.

The longer payment difficulties persist, the greater the risk of collections, defaults, and other financial complications. Recognizing these warning signs early may provide an opportunity to explore restructuring, settlement, or other relief options before the situation becomes more difficult to manage.

Warning Signs That MCA Withdrawals Are Becoming a Problem

MCA withdrawals are intended to provide a structured repayment process, but they can become a serious concern when they begin consuming too much of a business’s available revenue. What starts as a manageable obligation can gradually create cash flow pressure that affects daily operations and long-term financial stability.

Recognizing the warning signs early can help business owners take action before payment challenges lead to defaults, collections, or additional debt. The sooner these issues are identified, the more options may be available to improve cash flow and regain financial control.

Constant Cash Flow Shortages

One of the most common warning signs is a persistent shortage of available cash. If a business regularly struggles to maintain sufficient funds between deposits, MCA withdrawals may be placing too much strain on working capital.

Frequent cash flow shortages can make it difficult to plan for upcoming expenses and respond to unexpected business needs. Over time, this cycle can leave little financial flexibility to support normal operations or future growth.

Difficulty Covering Essential Business Expenses

When MCA payments consume a significant portion of incoming revenue, essential expenses may become harder to manage. Business owners may find themselves delaying payroll, vendor payments, inventory purchases, rent, utilities, or other operating costs.

These financial pressures can quickly affect both day-to-day operations and business relationships. If covering routine expenses becomes an ongoing challenge, it may indicate that current repayment obligations are no longer sustainable.

Using New Funding to Cover Existing MCA Payments

Another major warning sign is relying on new financing to cover existing MCA obligations. Some businesses take out additional merchant cash advances to maintain cash flow or avoid missed payments.

While this may provide temporary relief, it often increases overall repayment obligations and creates additional pressure on future revenue. As multiple withdrawals begin competing for the same cash flow, the risk of financial distress, defaults, and collections can grow significantly.

What Business Owners Can Do If Unexpected MCA Withdrawals Occur

Unexpected MCA withdrawals can create immediate financial pressure, especially when they interfere with payroll, vendor payments, or other essential operating expenses. While the situation can feel overwhelming, taking prompt action may help business owners better understand their obligations, stabilize cash flow, and identify potential solutions before the problem becomes more difficult to manage.

The most effective approach often begins with understanding the terms of the MCA agreement, evaluating the current financial impact, and exploring available relief options. Acting early may provide more flexibility and help prevent additional financial complications.

Review Your MCA Agreement Carefully

The first step is to review the merchant cash advance agreement in detail. Pay close attention to repayment terms, ACH authorization provisions, reconciliation clauses, default language, and any applicable fees.

Understanding exactly what was agreed to can help clarify whether withdrawals are occurring as expected under the contract. It can also help identify provisions that may affect future repayment obligations or available relief options.

Analyze Current Cash Flow and Account Activity

Business owners should closely examine recent bank activity and evaluate how MCA withdrawals are affecting overall cash flow. Reviewing deposits, operating expenses, payroll obligations, and other recurring costs can provide a clearer picture of the business’s financial position.

This analysis often helps identify whether current repayment obligations are sustainable or if withdrawals are creating ongoing cash flow shortages. Understanding the full financial impact is an important step toward developing an effective strategy.

Explore Available Relief and Restructuring Options

If MCA withdrawals are placing excessive strain on cash flow, it may be beneficial to explore available relief options. Depending on the circumstances, solutions may include restructuring existing obligations, negotiating modified payment arrangements, or pursuing settlement strategies.

Addressing the issue early often creates more opportunities to improve cash flow and avoid escalating financial pressure. Businesses that take action before defaults or collections occur may have greater flexibility when evaluating potential solutions.

Options for Businesses Struggling With MCA Payment Pressure

When MCA withdrawals begin creating ongoing cash flow challenges, many business owners assume they have no choice but to continue struggling with the existing payment structure. In reality, several relief options may be available depending on the company’s financial situation, the number of MCA obligations involved, and the terms of the agreements.

Exploring potential solutions early can often provide more flexibility and help prevent the situation from escalating into defaults, collections, or additional debt. Understanding the available options is an important step toward regaining control of business finances and creating a more sustainable path forward.

MCA Debt Restructuring Programs

MCA debt restructuring programs are designed to help businesses reduce payment pressure by modifying existing repayment arrangements. Depending on the circumstances, restructuring may involve negotiating lower payments, adjusting payment frequency, or creating a more manageable repayment structure.

The goal of restructuring is often to improve cash flow while allowing the business to continue operating. For companies facing multiple MCA obligations, restructuring may help create greater financial stability and reduce the strain caused by frequent withdrawals.

MCA Settlement Solutions

In some situations, MCA settlement may be an option for businesses experiencing significant financial hardship. Settlement typically involves negotiating with MCA providers to resolve a portion of the outstanding obligation through an agreed-upon payment arrangement.

Settlement solutions vary based on the facts of each case and are not appropriate for every business. However, when repayment challenges become severe, settlement discussions may provide an opportunity to address existing obligations and move toward a more stable financial position.

Professional Negotiation and Relief Assistance

Many business owners find it difficult to manage negotiations while simultaneously running their company and addressing cash flow concerns. Professional assistance can help evaluate available options, review MCA agreements, and develop a strategy based on the business’s specific circumstances.

Experienced negotiation support may also help businesses communicate more effectively with MCA providers and explore potential relief solutions. Taking action early often creates more opportunities to improve cash flow and avoid more serious financial complications.

Steps to Take Before MCA Withdrawals Create Larger Problems

When MCA withdrawals begin putting pressure on cash flow, taking action early can help prevent more serious financial challenges. Many business owners wait until payments become unmanageable, but addressing the situation sooner often creates more opportunities to improve cash flow and evaluate potential solutions.

A proactive approach can help businesses better understand their financial position, identify warning signs, and avoid the cycle of increasing payment pressure. The following steps can provide a starting point for regaining control before MCA withdrawals lead to larger operational or financial problems.

Review All Current MCA Obligations

Start by gathering all MCA agreements and reviewing the repayment terms for each obligation. Understanding payment amounts, withdrawal schedules, outstanding balances, and contract provisions can provide a clearer picture of the company’s overall financial commitments.

Monitor Bank Accounts and Cash Flow Closely

Regularly monitoring account activity can help identify cash flow shortages before they become critical. Tracking incoming revenue, operating expenses, and scheduled withdrawals allows business owners to anticipate potential challenges and make informed financial decisions.

Avoid Taking Additional MCA Funding

When cash flow becomes strained, taking out another merchant cash advance may seem like a quick solution. However, adding new repayment obligations often increases financial pressure and can make long-term recovery more difficult.

Seek Professional Guidance Early

Businesses experiencing ongoing MCA payment challenges may benefit from professional guidance before the situation escalates. Early intervention can help identify available relief options, evaluate repayment strategies, and create a plan to improve financial stability while maintaining business operations.

Taking Action Before MCA Withdrawals Damage Your Business

MCA withdrawals can quickly create financial pressure when they begin consuming too much of a company’s available cash flow. What starts as a manageable repayment obligation can gradually interfere with payroll, vendor payments, inventory purchases, and other essential operating expenses. The longer these challenges continue, the more difficult it may become to maintain financial stability and explore effective solutions.

Business owners often have more options available before missed payments, defaults, collections, or additional funding obligations create larger problems. Recognizing the warning signs early and taking proactive steps can help protect cash flow and position the business for a stronger financial future.

Why Early Action Often Creates More Options

Addressing MCA payment challenges early may provide greater flexibility when evaluating relief options. Businesses that take action before financial pressure becomes severe are often better positioned to explore restructuring opportunities, settlement strategies, or other solutions to improve cash flow.

Waiting too long can limit available choices and increase the risk of additional financial complications. Taking a proactive approach allows business owners to understand their situation and develop a plan before the problem becomes more difficult to manage.

Schedule a Free Consultation With MCA Shield

If MCA withdrawals are creating ongoing cash flow challenges for your business, now is the time to explore your options. The experienced team at MCA Shield can review your current obligations, analyze your financial situation, and help you understand the solutions available.

Schedule a free consultation today to learn how MCA Shield may help reduce payment pressure, improve cash flow, and create a more sustainable path forward for your business.